“This is your fund on drugs”

The Sequoia Fund’s (SEQUX) hefty sizing of Valeant Pharmaceuticals (VRX) dramatically changed the fund’s risk profile from historical norms. With the proper tools, allocators would have noticed this style drift back in Q2 2015 when Sequoia’s key factor exposures moved two to three times beyond historical averages. What’s more, allocators would have noticed a predicted volatility increase of 25% and a tracking-error increased 70%. Though this analysis would not have anticipated Valeant’s subsequent decline, it would have warned fund investors that Sequoia’s risk was out of the ordinary.

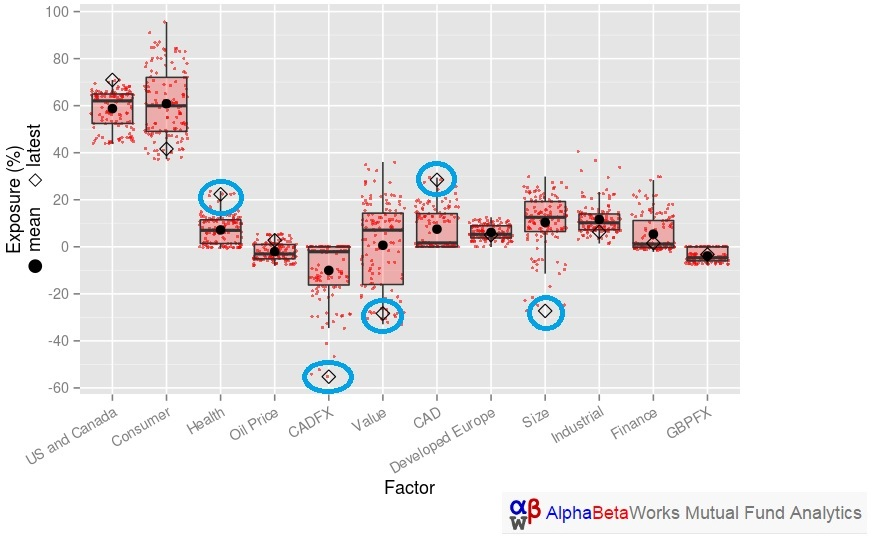

Sequoia Fund’s Risk Profile

Below is a chart of Sequoia’s major factor exposures, spanning a ten year history through June 2015:

Sequoia Fund (SEQUX) – Historical Factor Exposures

(Note that this analysis and our model do not include Valeant’s recent heightened volatility: we are using the AlphaBetaWorks Statistical Equity Risk Model as of 8/31/15 and SEQUX’s positions as of 6/30/2015. In short, we are looking at the world prior to Valeant’s subsequent downside volatility.)

Sequoia’s stock selection and allocation decisions result in certain factor bets such as market beta (“US and Canada”, above), other factors (Value, Size), and sectors (Consumer, Health). The red dots above represent factor exposures in a particular month, the red boxes represent two quartile deviations, and the diamonds denote current (i.e. 6/30/15) exposures. Several sectors/factors are circled for emphasis: they are current exposures as well as outliers versus history. More importantly, these outlying factor bets are the direct result of Sequoia’s large percentage ownership of Valeant.

The Impact of Valeant on Sequoia Fund’s Factor Exposures

We examined Sequoia Fund’s factor exposures with and without Valeant. We assumed that the pro forma Sequoia Fund without Valeant would have increased all other positions proportionally to make up for the void. For example, we increase Sequoia’s next-largest position (TJX) from 7.3% to 10.9%, and so on for all longs for the pro forma non-Valeant Sequoia portfolio.

Below is a chart comparing the most salient factor exposures of Sequoia Fund, with and without Valeant:

Sequoia Fund (SEQUX) – Factor Exposures With and Without Valeant (VRX)

Valeant has had a significant impact on Sequoia’s factor exposures. The factors with the highest delta are the same as those highlighted as outliers on the first chart above.

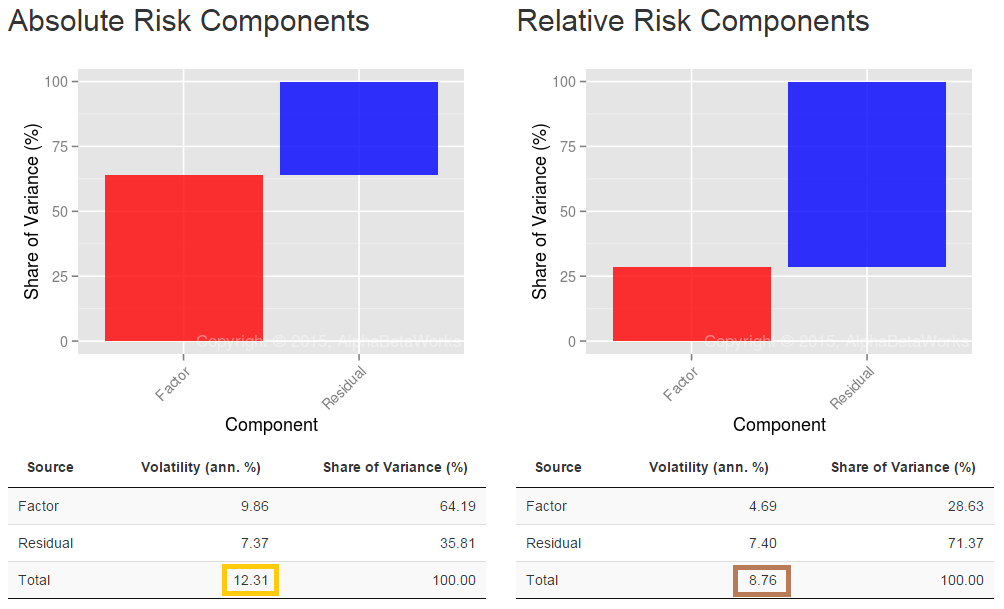

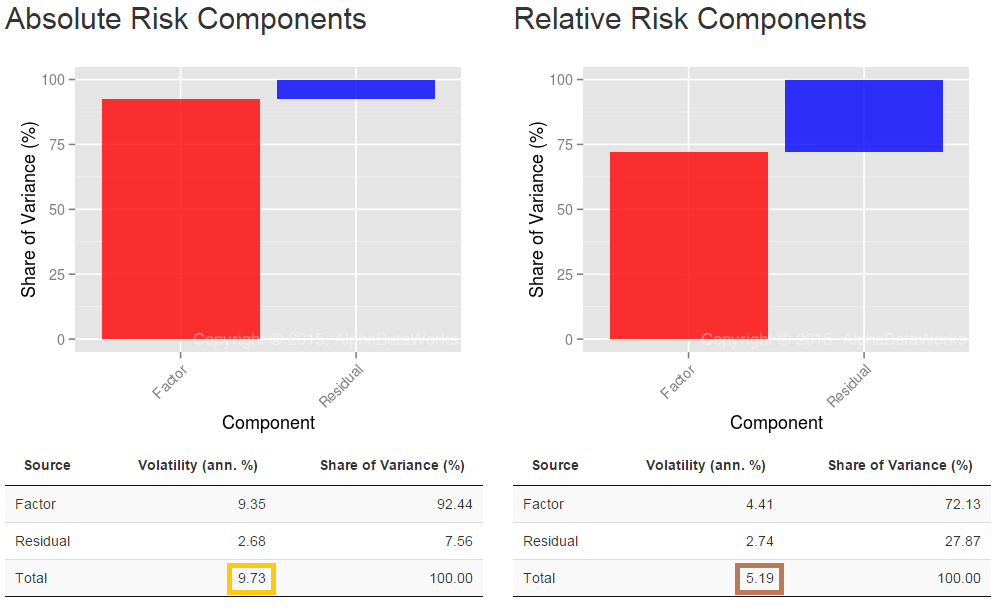

This is significant in several ways. First, the large Valeant holding increases Sequoia Fund’s overall volatility by 25%. Second, Sequoia’s tracking error is increased by its Valeant holding by 70%. Sequoia Fund volatility estimates with and without Valeant are below:

Sequoia Fund (SEQUX) with Valeant (VRX) – Absolute and Relative (to S&P 500) Estimated Risk

Sequoia Fund (SEQUX) without Valeant (VRX) – Absolute and Relative (to S&P 500) Estimated Risk

Valeant increases Sequoia’s overall predicted volatility (tracking error) by 26% (from 9.73% to 12.31%, annualized – gold boxes). Likewise, Valeant increases Sequoia’s tracking error by 69% (from 5.19% to 8.76% – brown boxes). Increases in both Absolute and Relative volatility are due to the incremental Residual Risk contribution of Sequoia’s large Valeant holding (graphically shown by the larger blue boxes in the “with VRX” charts, in contrast to smaller blue boxes in the “without VRX” charts).

Conclusions

In the end, this analysis is not about Sequoia or VRX. It is a single example of decisions that could have been avoided by a portfolio manager or questions that would have arisen to an allocator with the proper risk toolkit. Sequoia’s decision to make Valeant an outsized position did not go unnoticed from a risk standpoint. Increases in factor exposures of two to three times outside historical bounds were an early warning. The impact of this was increased predicted volatility – both on an absolute basis and relative to the S&P 500. A framework that warns of a fund taking large factor and idiosyncratic bets aids greatly in avoiding negative surprises.