Fee Harvesting is a Problem for All Asset Classes

To generate active returns in excess of its fees, an active fund must take some active risk. However, some managers passively manage their funds but charge active fees. Others become less active as they accumulate assets. This problem of closet indexing is not confined to mutual funds. Over a third of the long capital of U.S. hedge funds is invested too passively to warrant a typical 1.5/15% fee structure, even if the funds’ managers are highly skilled. Investors could replace closet indexers with passive vehicles or truly active skilled managers and improve performance.

Closet Indexing Background

Two of our earlier articles explored past and current mutual fund closet indexing:

One article analyzed historical risk and performance of U.S. mutual funds. It discovered that over a quarter (26%) of the funds have been so passive that, even after exceeding the information ratios of 90% of their peers, they would still not be worth the 1% mean management fee.

The other article addressed current risk and predicted volatility of U.S. mutual funds. It found that over two thirds (70%) of their capital is currently taking so little active risk that it will fail to merit the 1% mean management fee, even if the funds’ managers are highly skilled.

This article surveys long portfolios of hedge funds. We analyze current and historical long positions of approximately 300 concentrated medium and lower turnover U.S. hedge funds, identifying those that are unlikely to earn their fees in the future given their current active risk. We then quantify the problem of closet indexing for a typical hedge fund investor.

How Much Active Risk is Needed to Earn a Fee?

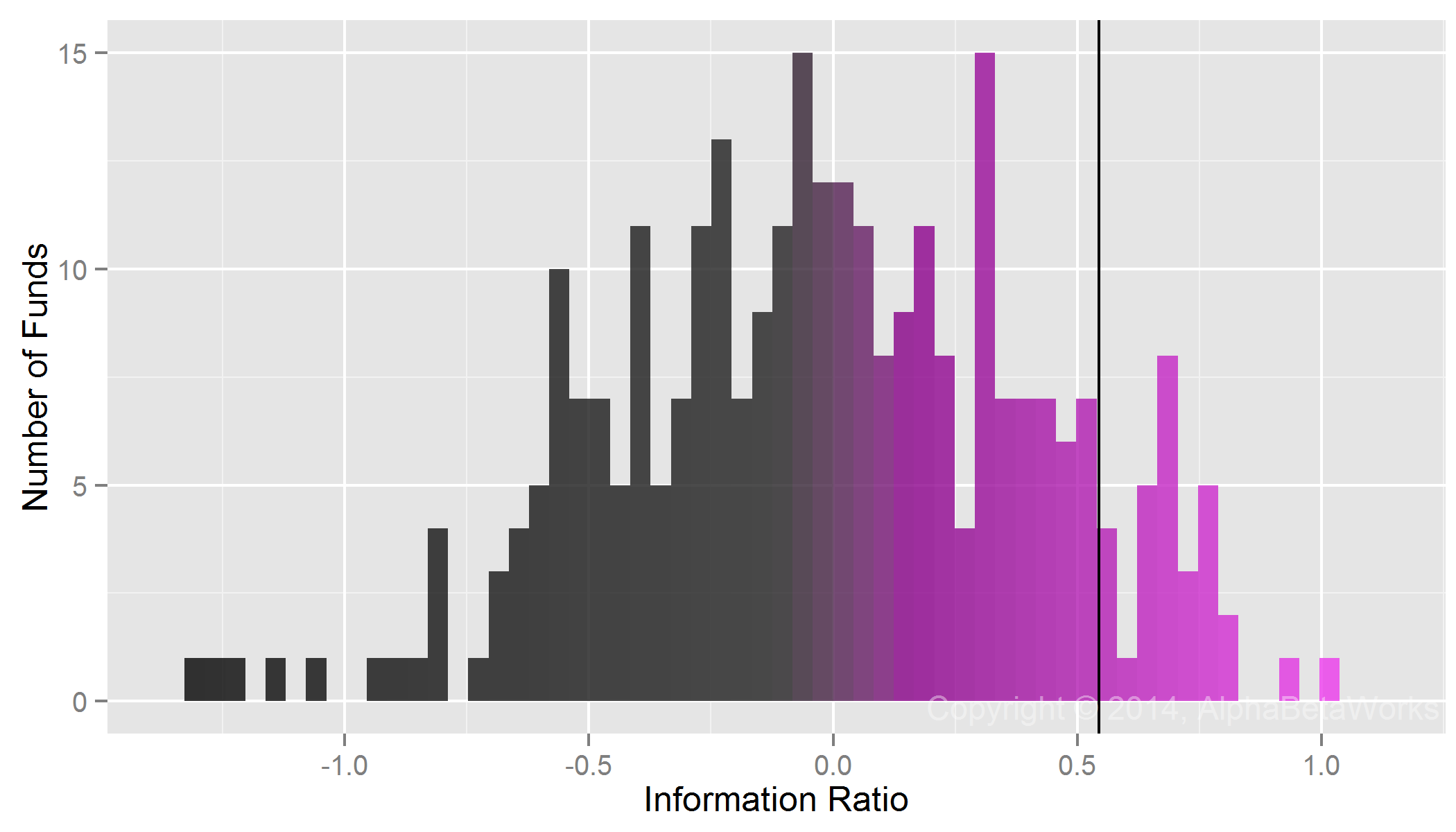

The Information Ratio (IR) is a measure of active return relative to active risk (tracking error). The best-performing 10% of U.S. hedge funds’ long portfolios achieve IR’s of 0.54 and higher; 90% achieve IR’s below 0.54:

U.S. Hedge Fund Information Ratio Distribution – Long Positions

If a fund’s long portfolio exceeds the performance of 90% of its peers and achieves an IR of 0.54, then it needs tracking error above 1.85% to generate active return above 1%.

What active return will cover a typical fee? We make conservative assumptions that funds’ long equity portfolios are burdened with 1.5% management fee and 15% incentive allocation. Assuming 7% expected market return, the mean fee is 2.55%.

If all funds were able to achieve the 90th percentile of IR, they will need annual tracking error above 4.7% to earn this estimated mean fee and generate a positive net active return.

Hedge Fund Active Risk

Tracking error is due to active risks a fund takes: security selection risk due to stock picking and market timing risk due to variation in factors bets. We applied the AlphaBetaWorks Statistical Equity Risk Model to funds’ historical and latest holdings and estimated their historical and future tracking errors. Tracking errors were calculated relative to fund-specific benchmarks that represent each fund’s unique passive risk profile.

Over a tenth (33) of the funds have such low historical tracking errors that, even if they exceeded the performance of 90% of their peers, they would have failed to merit the 2.55% estimated mean fee:

U.S. Hedge Fund Historical Tracking Error Distribution – Long Positions

Over a fifth (61) of the funds have such low estimated future tracking errors that, even if they exceed the performance of 90% of their peers, they will fail to merit the 2.55% estimated mean fee:

U.S. Hedge Fund Estimated Future Tracking Error Distribution – Long Positions

While there is less closet indexing among hedge funds than among mutual funds, the fees that hedge funds charge are significantly higher — to say nothing of the higher expectations that these higher fees warrant. When practiced by hedge funds, closet indexing is all the more egregious.

Capital-Weighted Hedge Fund Closet Indexing

Larger hedge funds are more likely to engage in closet indexing. While approximately 20% of hedge funds surveyed have estimated future tracking errors below 4.7%, they represent nearly 40% of assets ($207 billion out of the $391 billion total in our sample). Therefore, more than a third of hedge fund long capital will not earn the 2.55% estimated mean fee, even when the managers are skilled.

U.S. Hedge Fund Capital Estimated Future Tracking Error Distribution – Long Positions

The assumption of all funds exceeding historical IR’s of 90% of their peers is unrealistic. In practice, a portfolio of large hedge funds, built without attention to closet indexing, may be doomed to generate negative active returns, regardless of the managers’ skills. The 2.55% fee cited here is the estimated mean. Plenty of closet indexers charge more on their long equity portfolios and plenty of investors who remain with them stand to lose more.

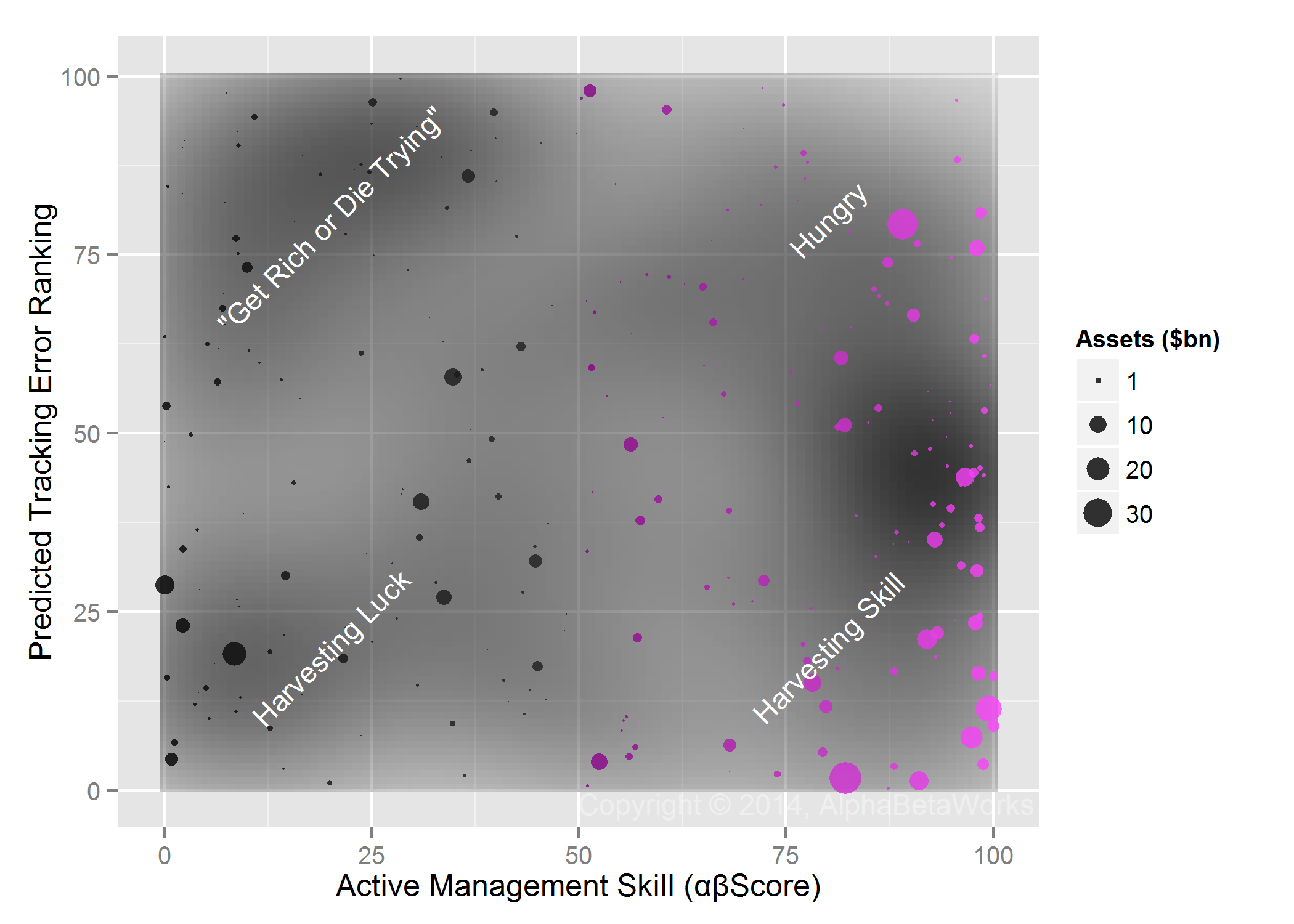

A Map of Hedge Fund Skill and Activity

Our previous article discussed the evolution of skilled managers’ utility curves as an explanation for their reluctance to take risk. As a manager accumulates assets, fee harvesting becomes increasingly attractive. The map of U.S. hedge fund active management skill and activity below illustrates that large skilled funds tend to be relatively less active:

U.S. Hedge Fund Active Management Skill and Activity – Long Positions

Conclusions

- 20% of long U.S. hedge fund portfolios surveyed are currently so passive that, even after exceeding the information ratios of 90% of their peers, they will still fail to merit a typical fee.

- 39% of long U.S. hedge fund capital surveyed will fail to merit a typical fee, even if its managers are highly skilled.

- Investors must monitor the evolution of their hedge fund managers towards closet indexing and mitigate fee harvesting.

- A typical investor may be able to replace over a third of long hedge fund capital with passive vehicles or active skilled managers, improving performance.