Managers Are Skilled in Specific Areas, Seldom Excellent at Everything

Investors typically treat all ideas of excellent managers with equal deference. This is usually a mistake – even the most skilled managers are seldom equally skilled in all areas. Skilled managers may derive all of their risk-adjusted performance from a few specific areas, and under-perform in others.

Greenlight Capital – Long Equity Security Selection

David Einhorn’s Greenlight Capital is one of the best-known value hedge funds. The long-term performance of the fund has attracted a media and investor following. Many analysts advocate buying a stock solely because it has been purchased by Greenlight Capital; many investors do.

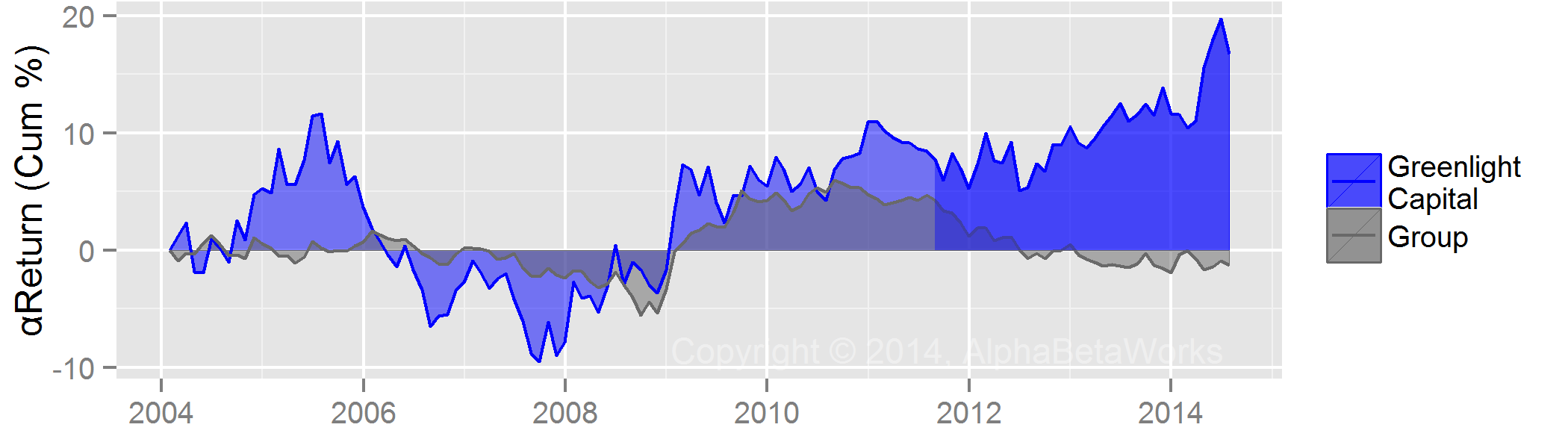

The risk-adjusted return of Greenlight Capital’s long equity portfolio, estimated from the firm’s 13F filings, is indeed excellent. We estimate a 20% cumulative return from security selection (stock picking) over the past 10 years. This is Greenlight’s αReturn, a metric of security selection performance – the estimated annual percentage return a fund would have generated in a flat market:

Greenlight Capital Security Selection Return – Long Equity Portfolio

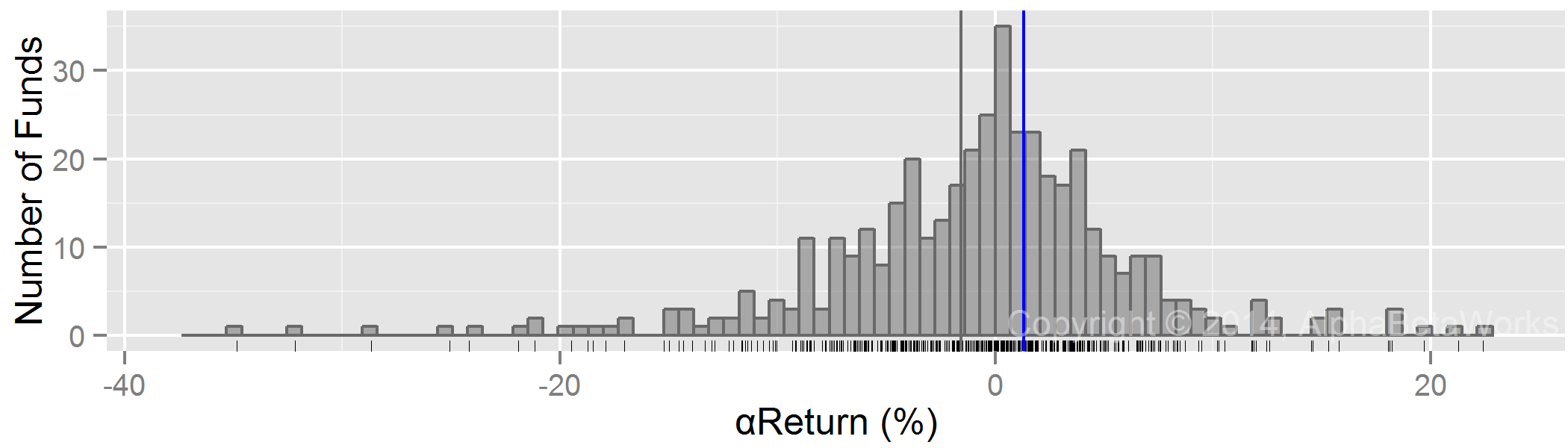

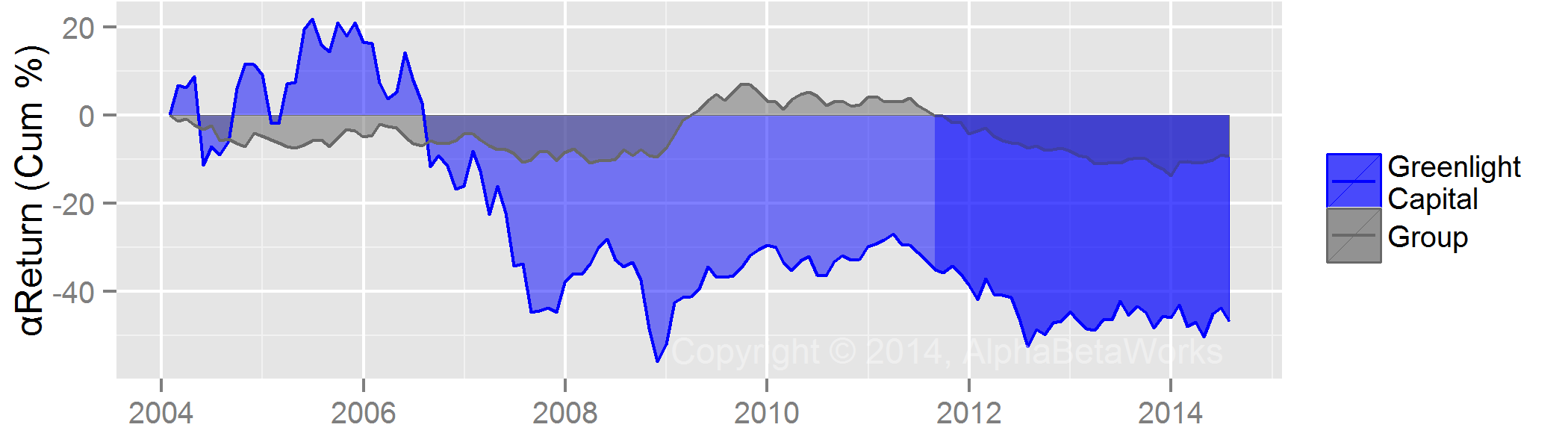

By contrast, the long portfolios of medium turnover U.S. hedge funds generated negative security selection return (αReturn) over the same period. If the market had been flat for the past 10 years, the average fund would have lost money. Greenlight Capital’s αReturn topped two thirds of its peers’:

Greenlight Capital and Peers Security Selection Return Distribution – Long Equity Portfolio

Technology Sector Performance

Was Greenlight Capital equally effective selecting securities in all sectors? Or should investors be wary of some ideas, in spite of the outstanding overall security selection record?

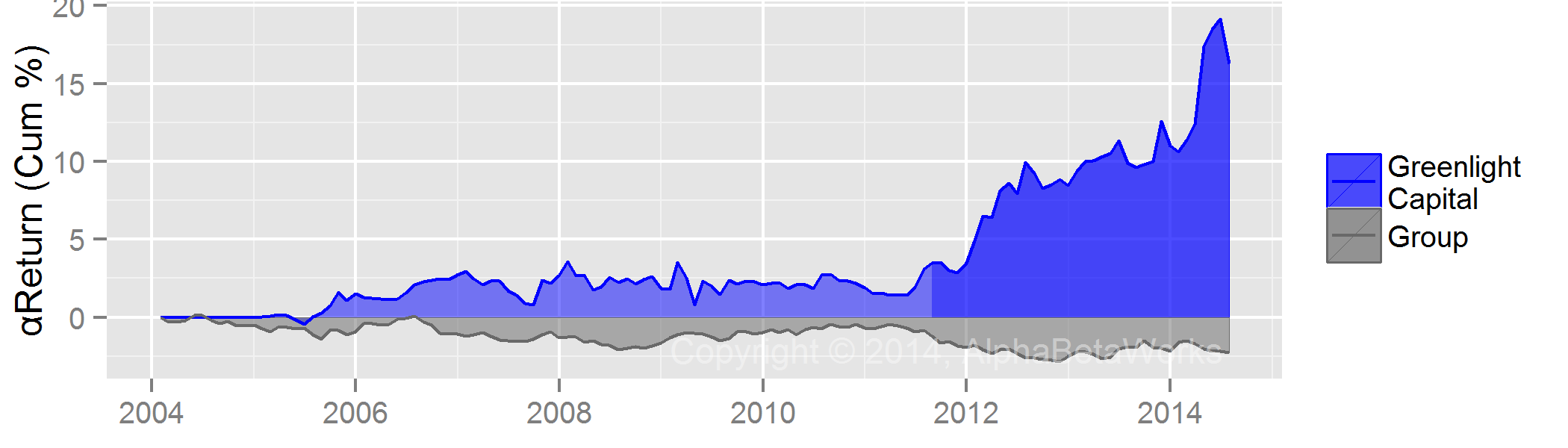

It turns out that the αReturn of the overall fund came primarily from a single sector – Technology:

Greenlight Capital Technology Sector Security Selection Return Contribution – Long Equity Portfolio

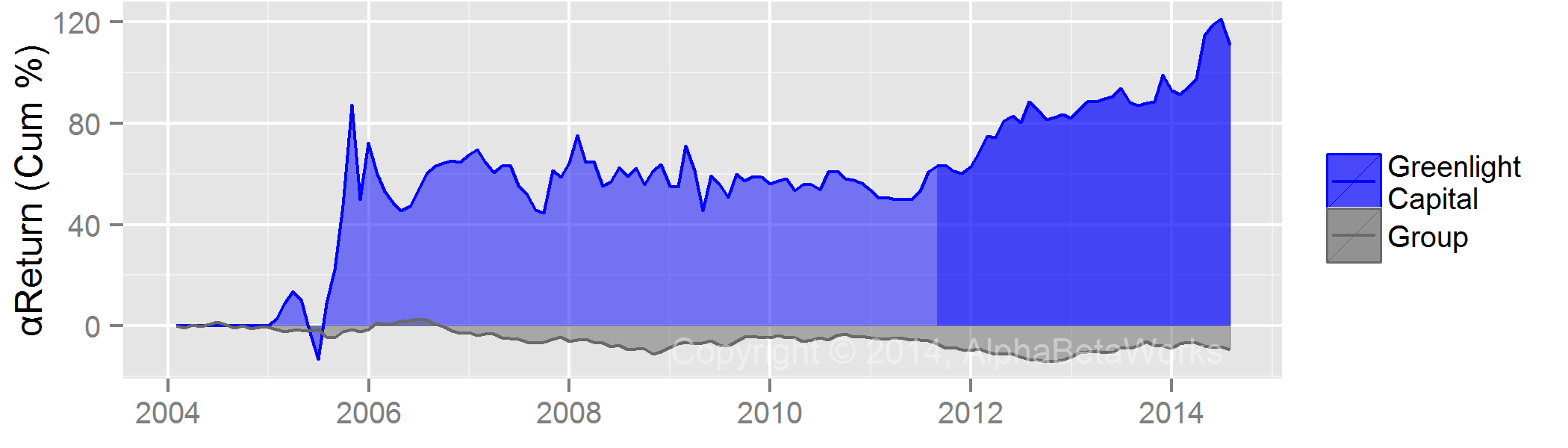

Viewed in isolation, the technology portfolio generated over 100% αReturn (risk-adjusted return from stock picking). If markets had been flat for the past 10 years, Greenlight Capital’s long technology portfolio would have generated over 100%:

Greenlight Capital Security Selection Return – Long Technology Equity Portfolio

Non-Technology Sector Performance

Since the entire 10-year αReturn of Greenlight Capital came from its technology positions, other sectors contributed zero αReturn.

Therefore, investors should not treat all picks, positions, and ideas of the fund equally. For instance, investors may want to stay clear of the fund’s healthcare picks. We estimate that if markets had been flat for the past 10 years, Greenlight’s long healthcare equity portfolio would have lost over 40%:

Greenlight Capital Security Selection Return – Long Healthcare Equity Portfolio

Investors usually treat all ideas of excellent managers as equally excellent. This is a mistake. Even the most skilled stock pickers are rarely equally skilled in all industries. Often, their picks in some industries predictably underperform.

Current Holdings

Greenlight’s performance in these sectors results from a number of positions over time and not from a few outliers. Their top current holdings in the technology sector, an area of exceptional skill, are:

| MU | Micron Technology, Inc. |

| MRVL | Marvell Technology Group Ltd. |

| AAPL | Apple Inc. |

| SUNE | SunEdison, Inc. |

| EMC | EMC Corporation |

Based on Greenlight’s risk-adjusted performance in this sector, these equities are likely to generate positive risk-adjusted returns in the future.

Greenlight’s holdings in the health sector, an area of weakness, are:

| CI | Cigna Corpora |

| AET | Aetna Inc. |

| XON | Intrexon Corporation |

Based on Greenlight’s risk-adjusted performance in this sector, these holdings are unlikely to match the risk-adjusted performance of the rest of the portfolio and may generate negative returns in a flat market.

Conclusions

- Investors wrongly assume that outstanding investment managers are skilled in all areas.

- Investment managers are rarely skilled in all areas.

- Most skilled managers derive the bulk of their risk-adjusted returns from a few specific areas of skill.

- Most skilled managers have areas of weakness.

- Even highly skilled managers may have areas where they can be predicted to generate negative risk-adjusted returns.

Pingback: Friday links: flexible asset allocations | Abnormal Returns

Thanks for featuring our quote of the day at abnormalreturns.com.

Do you have a list or database of which managers generate the most alpha on a sector by sector basis? I.e. who has the best risk-adjusted performance in energy or consumer discretionary etc.

Yes, we collect this data and it is part of our database, screening tools, and certain reports.

Is there anyway to see how are the top ranked managers in certain sectors? Do you think youll do a post which covers that perhaps? Would be very interesting

Thank you for the suggestion. This idea does come up. The trick is balancing the benefits our subscribers get from exclusive access to manager skill insights with the benefits of wider awareness of our thought leadership in this area.

We are looking for ways to publicly release actionable insights on some of the top-performing managers in specific sectors while preserving the value of our exclusive content. Please stay tuned…