U.S. hedge funds share a few systematic and idiosyncratic long bets – a phenomenon called “crowding.” Hedge fund crowding within specific sectors can be heavy; bets on exploration and production (E&P) companies are particularly crowded. Hedge fund E&P bets are the subject of this article. Eight stocks are responsible for three quarters of the herding.

Crowding is costly to investors, fund managers, and allocators: over the past 10 years the aggregate hedge fund E&P portfolio underperformed the market E&P portfolio by 23% while taking more risk. The risk-adjusted return was even worse – a loss of 52%.

Identifying Hedge Fund E&P Crowding

To evaluate hedge fund (HF) exploration and production (E&P) herding, we followed the approach of our earlier work on aggregate and sector-specific hedge fund crowding: We created an aggregate position-weighted portfolio (HF E&P Aggregate) consisting of all exploration and production long equity positions reported by over 400 U.S. hedge funds with medium to low turnover. We then evaluated HF E&P Aggregate’s risk relative to the capitalization-weighted portfolio of E&P equities (Market E&P Aggregate) using AlphaBetaWorks’ Statistical Equity Risk Model.

Crowded E&P Stocks Underperform

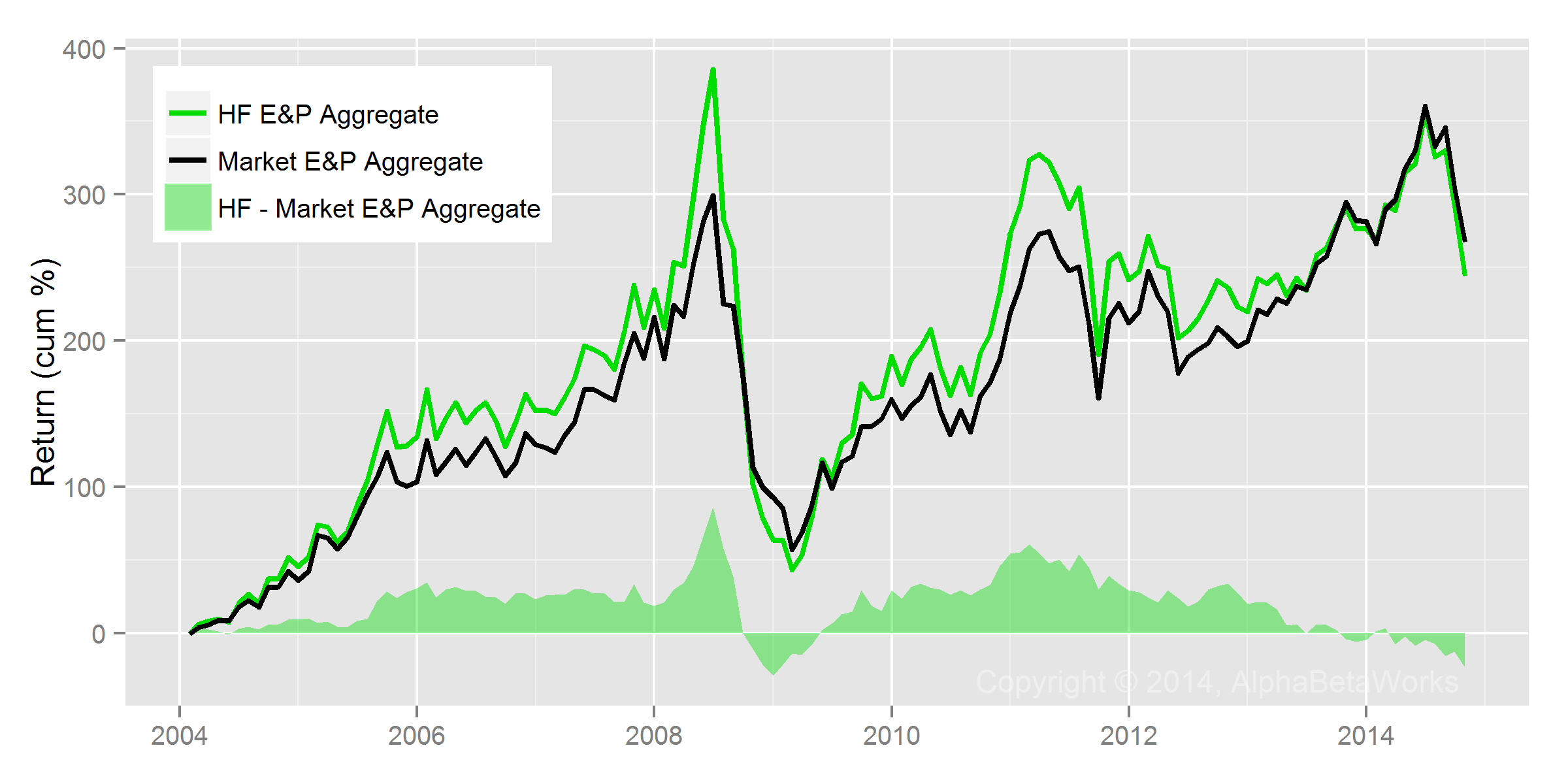

Crowding hurts performance. HF E&P Aggregate had poor returns following the peak of the last energy cycle in 2008. Consequently, understanding Hedge Fund E&P crowding is vital to investors, fund managers, and allocators.

When the broad market and the E&P sector are doing well, crowded hedge fund E&P stocks generally outperform. However, these stocks generally underperform in the down cycle. This is a tell-tale sign of flocking to higher-risk stocks. This crowding towards higher market and sector betas is consistent with the aggregate systematic crowding of hedge funds:

Historical Return for Hedge Fund E&P Aggregate vs. Market E&P Aggregate

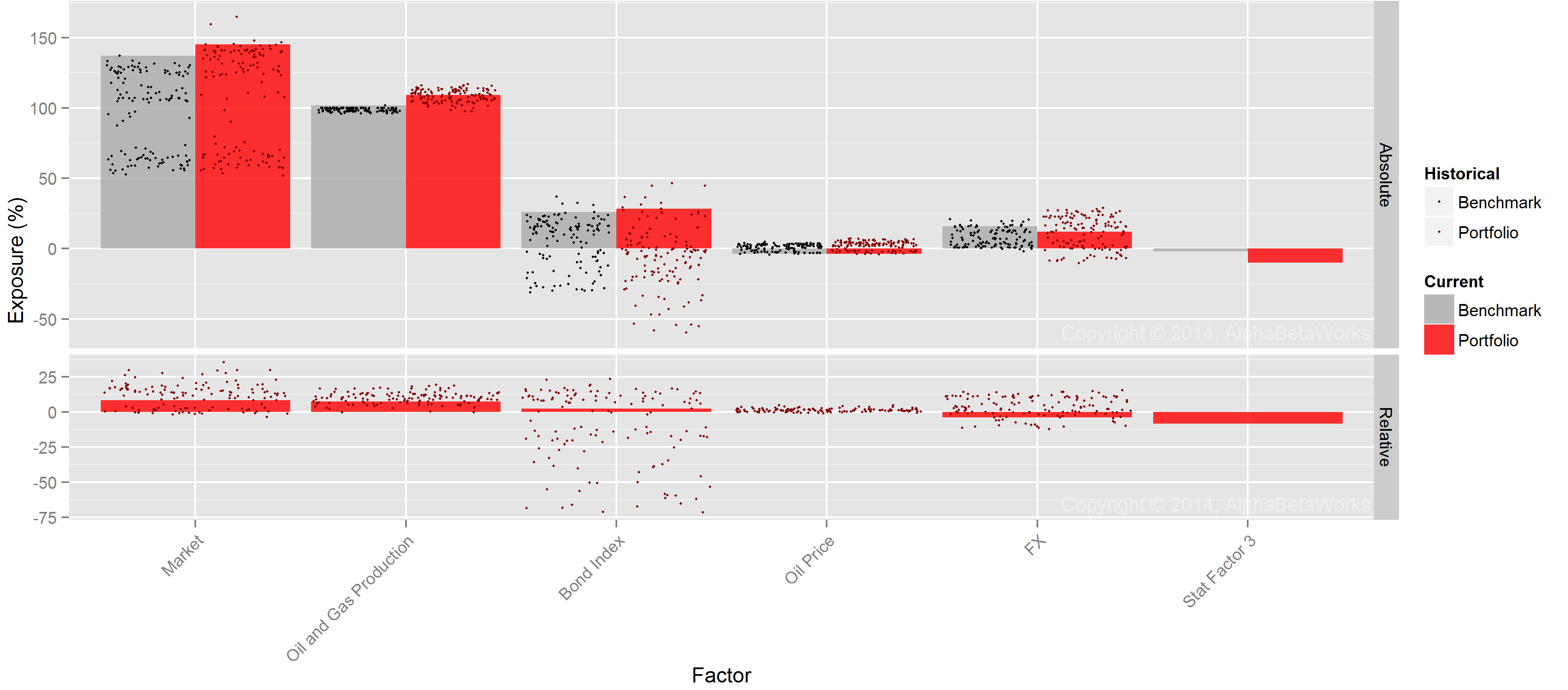

Indeed, we will see later that hedge fund E&P aggregate has both higher market exposure (market beta) and higher E&P sector exposure (E&P sector beta) than the market E&P Aggregate.

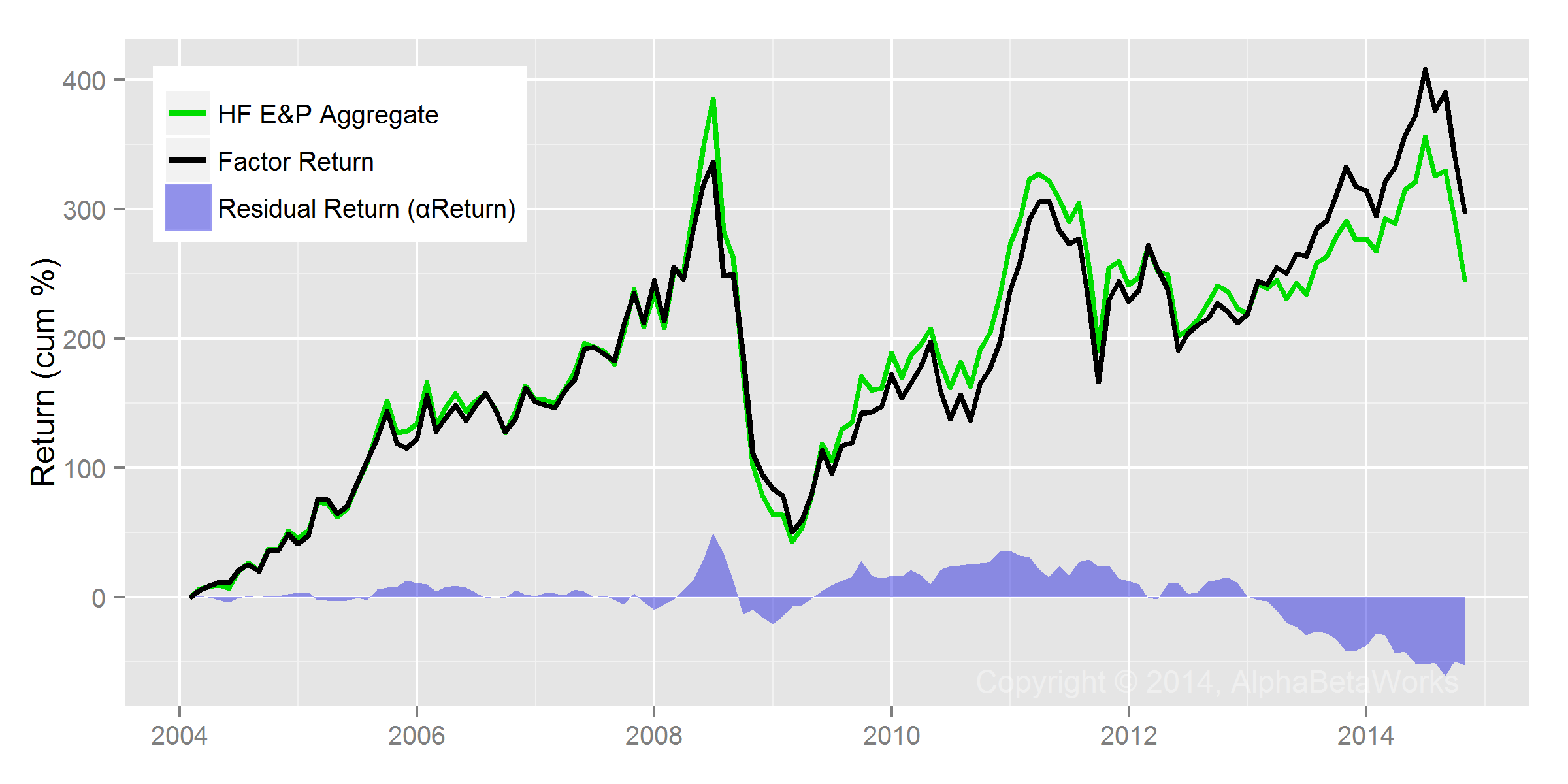

When we adjust for the systematic (factor) risk, we discover that the residual return of HF E&P aggregate due to security selection is even worse. Investors would have made 52% more over the past 10 years if they had invested in an ETF portfolio with similar factor risk:

Historical Hedge Fund E&P Aggregate, Factor, and Residual Returns

Hedge Fund E&P Risk

HF E&P Aggregate has a 5.0% estimated future tracking error relative to Market E&P Aggregate, primarily due to stock-specific bets:

Sources of Relative Risk for Hedge Fund E&P Aggregate

| Source | Volatility (%) | Share of Variance (%) |

| Factor | 2.77 | 24.67 |

| Residual | 4.31 | 75.33 |

| Total | 4.96 | 100.00 |

The 5.0% tracking error means that HF E&P Aggregate’s annual return is forecasted to differ from Market E&P Aggregate’s by less than 5.0% two thirds of the time.

Hedge Fund Factor (Systematic) E&P Crowding

On the chart below, HF E&P Aggregate’s factor exposures (red) are similar to Market E&P Aggregate’s (gray), but tend to be higher. Hedge Funds tend to invest in names with higher market and sector betas, perhaps as a logical consequence of their compensation structure:

Hedge Fund E&P Aggregate’s Exposure to Significant Risk Factors

Hedge Fund Residual (Idiosyncratic) E&P Crowding

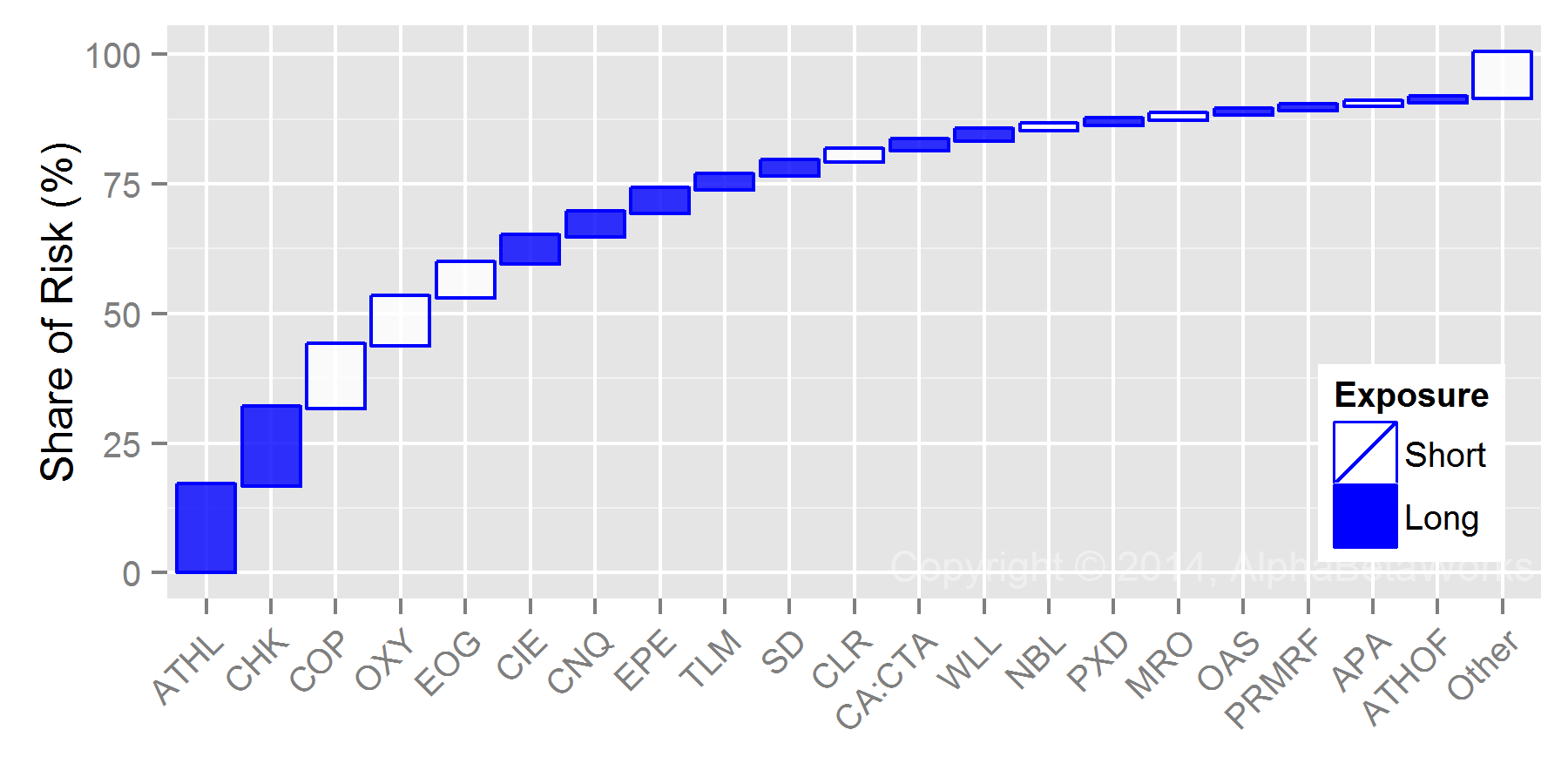

Over 75% of the relative risk of HF E&P Aggregate is due to stock-specific (residual) bets. Below are the sources of HF E&P Aggregate’s relative residual variance. Three quarters of the estimated relative residual risk is due to only eight stocks:

Stocks Contributing Most to Relative Residual Variance of Hedge Fund E&P Aggregate

As with HF Energy Aggregate, some of the largest bets are not the stocks hedge funds own, but the stocks they don’t own. (For example, hedge funds are underweight COP, OXY, and EOG.) The crowded bets are likely to deliver negative risk-adjusted returns in flat or declining oil and gas producer cycle.

| Position (%) | |||||

| Symbol | Name | HF E&P Aggregate |

Market E&P Aggregate |

Relative | Share of Risk (%) |

| ATHL | Athlon Energy, Inc. | 7.95 | 0.54 | 7.41 | 16.64 |

| CHK | Chesapeake Energy Corporation | 9.63 | 2.41 | 7.23 | 14.96 |

| COP | ConocoPhillips | 0.51 | 12.30 | -11.79 | 12.21 |

| OXY | Occidental Petroleum Corporation | 0.36 | 9.33 | -8.97 | 9.18 |

| EOG | EOG Resources, Inc. | 0.87 | 7.46 | -6.60 | 6.65 |

| CIE | Cobalt International Energy, Inc. | 3.31 | 0.87 | 2.44 | 5.11 |

| CNQ | Canadian Natural Resources Limited | 6.06 | 0.00 | 6.06 | 4.58 |

| EPE | EP Energy Corp. Class A | 11.31 | 0.66 | 10.65 | 4.55 |

| TLM | Talisman Energy Inc. | 3.96 | 0.00 | 3.96 | 2.69 |

| SD | SandRidge Energy, Inc. | 2.67 | 0.41 | 2.26 | 2.68 |

| CLR | Continental Resources, Inc. | 0.09 | 3.43 | -3.34 | 2.09 |

| CA:CTA | Crocotta Energy Inc. | 0.18 | 0.00 | 0.18 | 1.93 |

| WLL | Whiting Petroleum Corporation | 4.08 | 1.12 | 2.95 | 1.92 |

| NBL | Noble Energy, Inc. | 0.33 | 3.29 | -2.96 | 1.09 |

| PXD | Pioneer Natural Resources Company | 6.12 | 3.83 | 2.28 | 1.02 |

| MRO | Marathon Oil Corporation | 0.08 | 3.13 | -3.05 | 0.95 |

| OAS | Oasis Petroleum Inc. | 2.48 | 0.66 | 1.83 | 0.84 |

| PRMRF | Paramount Resources Ltd. Class A | 1.26 | 0.00 | 1.26 | 0.81 |

| APA | Apache Corporation | 1.63 | 4.49 | -2.86 | 0.78 |

| ATHOF | Athabasca Oil Corporation | 1.13 | 0.00 | 1.13 | 0.77 |

Of course, the poor long-term performance of the HF E&P aggregate does not mean that some individual equities will not do well. In fact, in the third quarter of 2014, ATHL was acquired. With half of the shares owned by hedge funds, ATHL was one of the largest positions of HF E&P Aggregate and the top idiosyncratic bet.

Summary

- Hedge Fund Exploration and Production (E&P) Aggregate tends to have higher risk than Market E&P Aggregate.

- Crowded Hedge Fund E&P stocks tend to underperform market aggregate over the long-term, in spite of higher risk.

- Crowded Hedge Fund E&P stocks tend to generate negative risk-adjusted returns.

- There is both factor (systematic/market) and residual (idiosyncratic/security-specific) crowding of long hedge fund E&P portfolios.

- Over 80% of recent crowding is attributable to eight stocks: ATHL, CHK, COP, OXY, EOG, CIE, CNQ, and