And The Flaws of Blind Fund-Following Strategies

Numerous financial data and analytics vendors peddle hedge fund tracking strategies and content. Much of this data is hazardous to investors – Hedge fund survivor bias, a special case of the pervasive survivorship bias, is its key flaw. This artifact overstates nominal fund returns by a fifth and conceals mediocre risk-adjusted performance records.

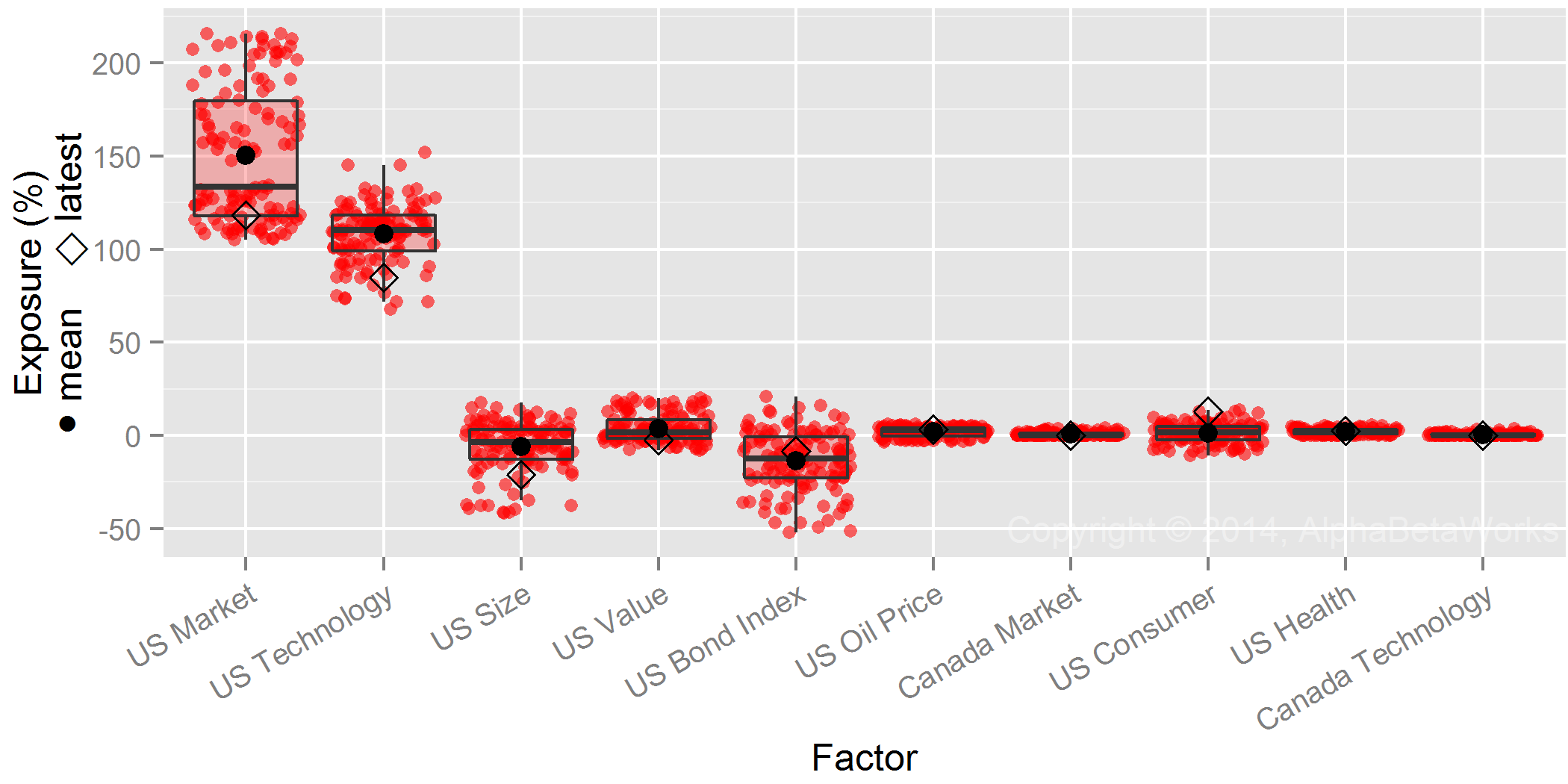

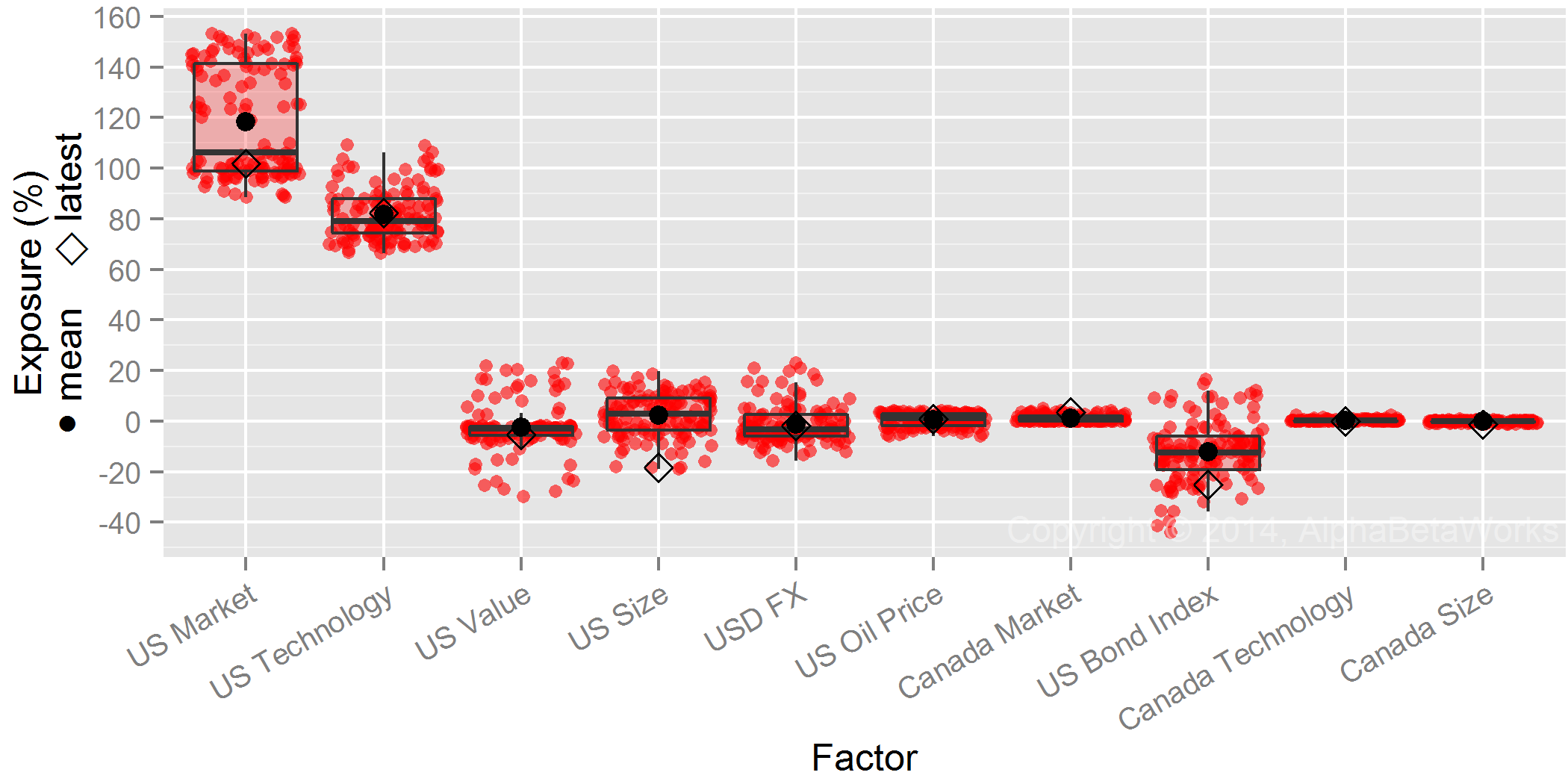

This post is technical, but it illustrates an important phenomenon and sets up the foundation for upcoming articles. We analyze the long equity portfolios of approximately 1,000 medium and lower turnover non-quantitative hedge funds active over the past 10 years (HF Aggregate). This dataset spans the long portfolios of all non-quantitative hedge funds active over the past 10 years that are tractable using 13F filings.

HF Aggregate consists of two approximately equal sub-sets: HF Surviving Aggregate and HF Defunct Aggregate. HF Surviving Aggregate, similar to the datasets of many vendors, gives a deeply misleading picture of average hedge fund performance. Our HF Aggregate corrects this by including HF Defunct Aggregate – funds that stopped filing 13Fs as their U.S. assets dropped below $100 million.

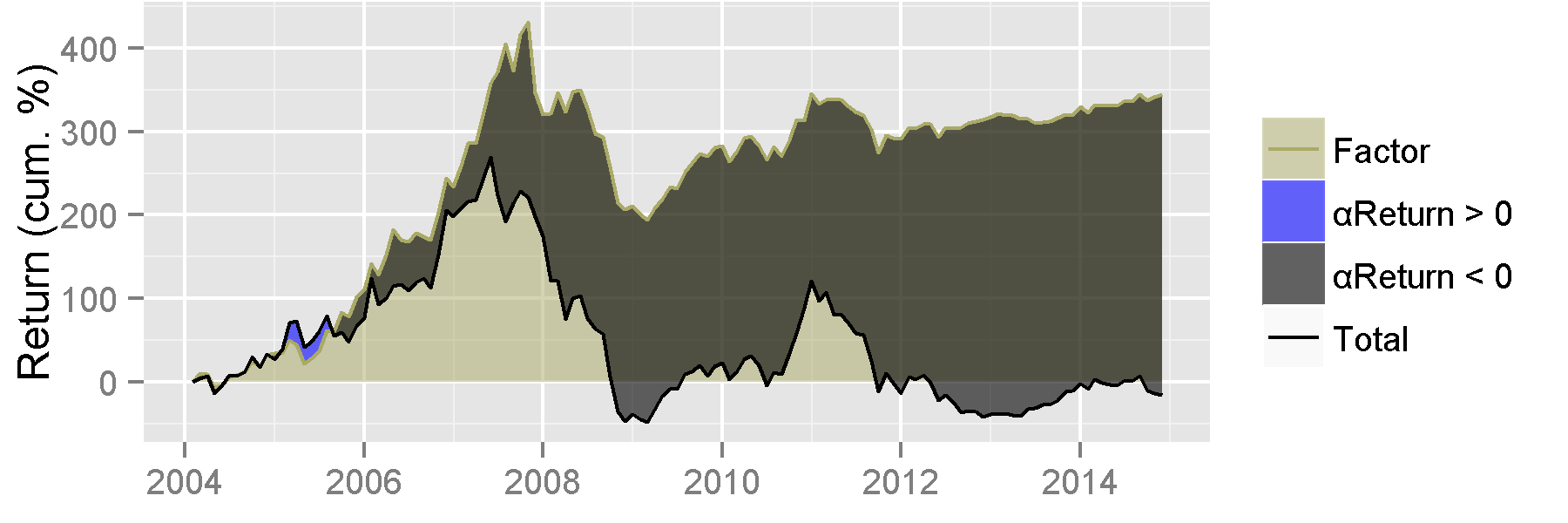

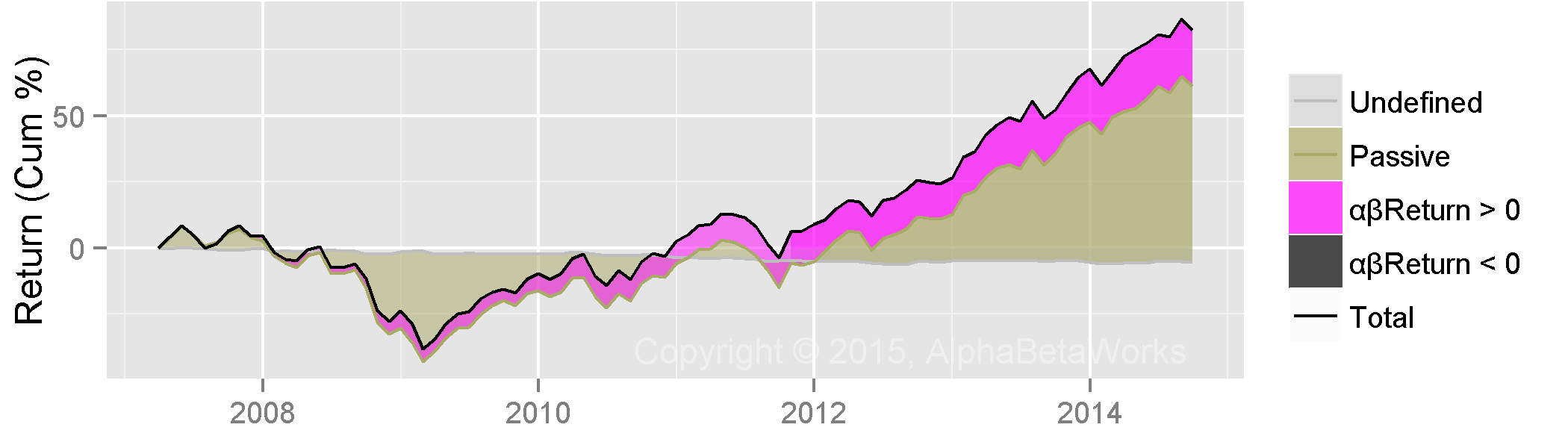

All Hedge Fund Performance

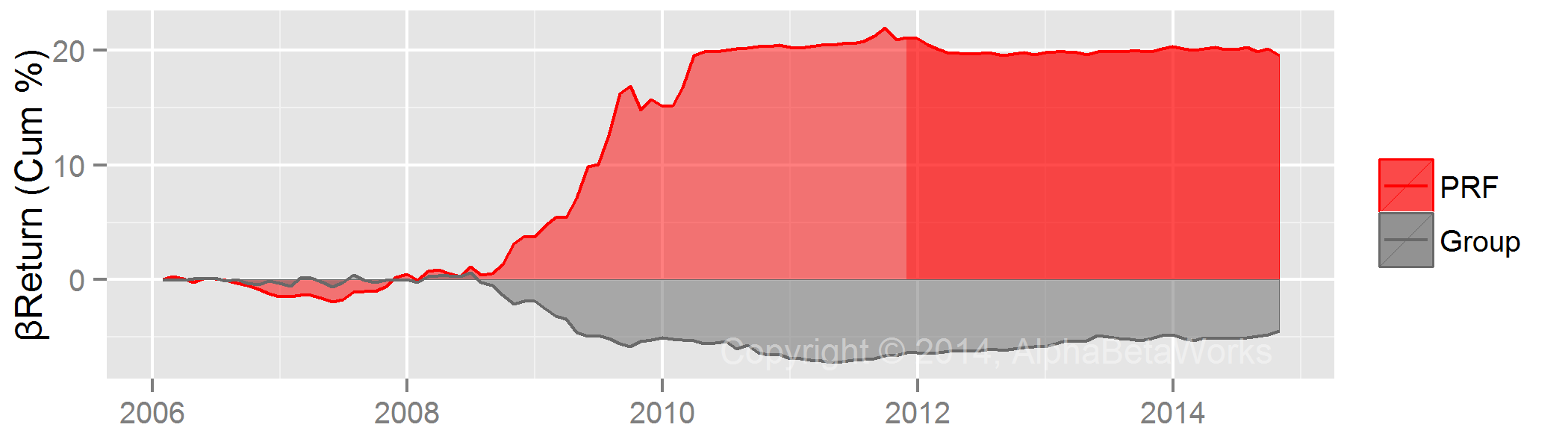

We compare HF Aggregate to Factor Portfolio – a portfolio with matching factor (systematic) risk. Factor Portfolio captures the return investors would have realized if they had passively invested in ETFs and index futures with the same risk as HF Aggregate. We do this to calculate security selection (stock picking) returns of HF Aggregate.

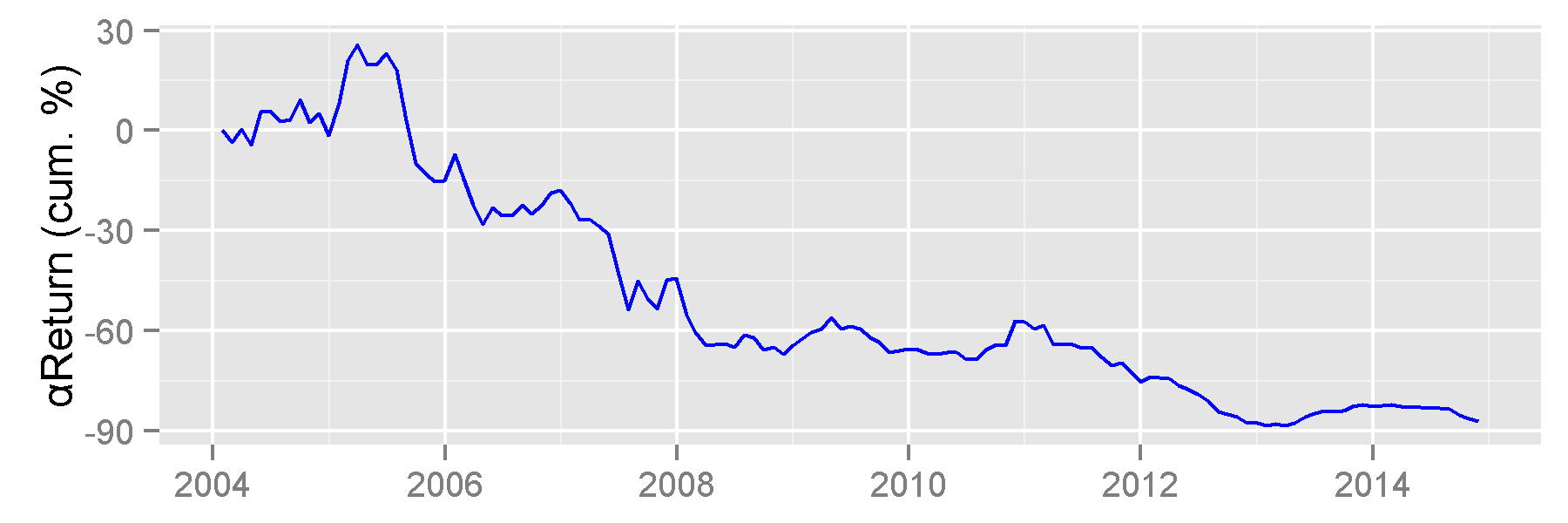

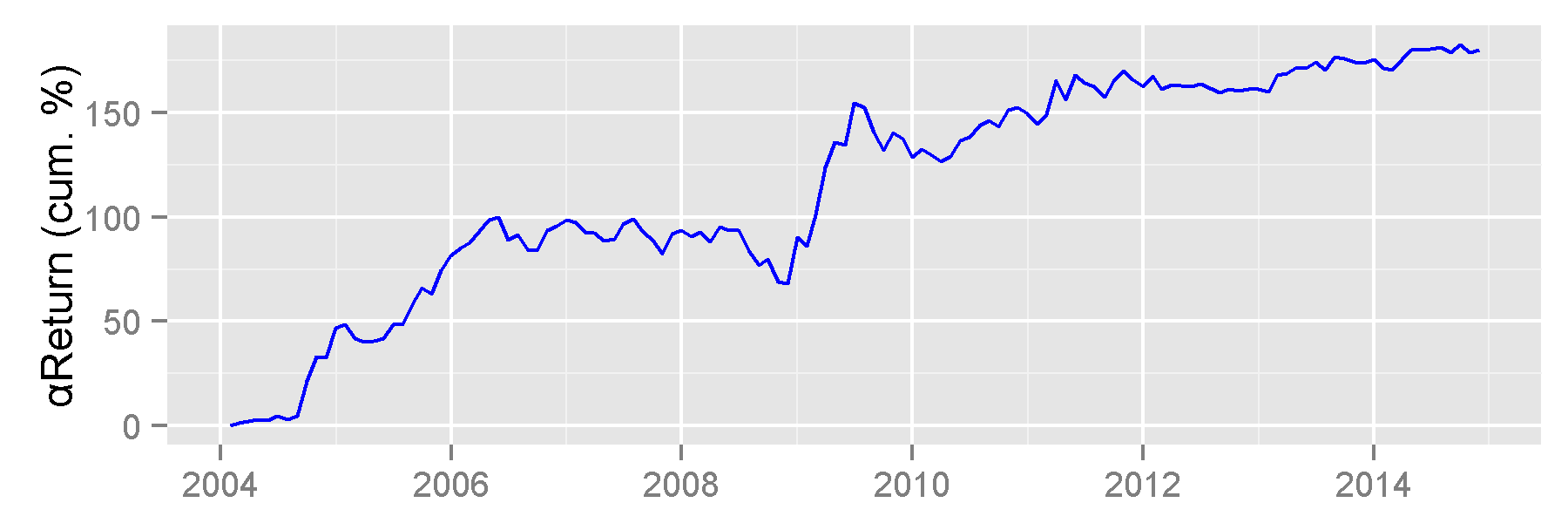

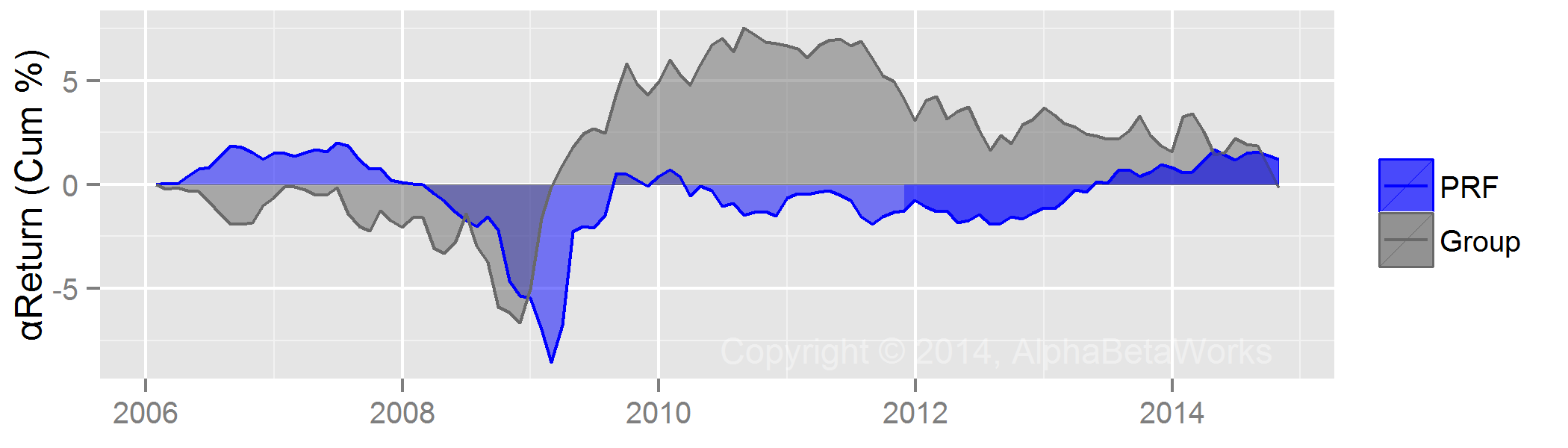

With the exception of the 2009-2011 period, HF Aggregate generated negative returns from security selection. AlphaBetaWorks’ measure of security selection performance is αReturn – outperformance relative to the Factor Portfolio. αReturn is also the return HF Aggregate would have generated if markets were flat. Since 2011, HF Aggregate’s αReturn was -2%. If markets had been flat, the average medium-turnover long hedge fund portfolio would have lost 2% from its long portfolio. Including the effects of compounding with factor returns, αReturn was -3%.

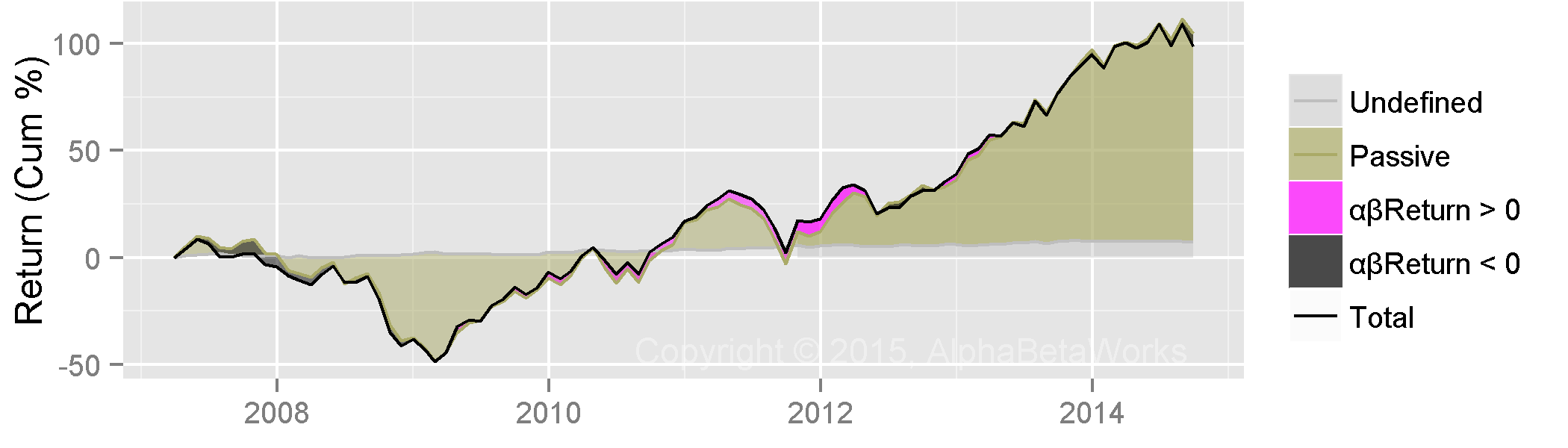

Putting these elements together, the chart below compares HF Aggregate’s performance (green) to the Factor Portfolio (black). The security selection performance, or αReturn (blue), is the difference between the two. This is the true long performance of the average hedge fund:

All Medium Turnover U.S. Hedge Fund Long Portfolios: Factor, Residual, and Total Returns

|

Performance (%) |

||

|

Annualized |

10-year | |

| Total |

8.48 |

133.57 |

| Factor |

8.60 |

136.39 |

|

Total – Factor |

-0.12 |

-2.82 |

Survivor Hedge Fund Performance – Survivorship Bias in Action

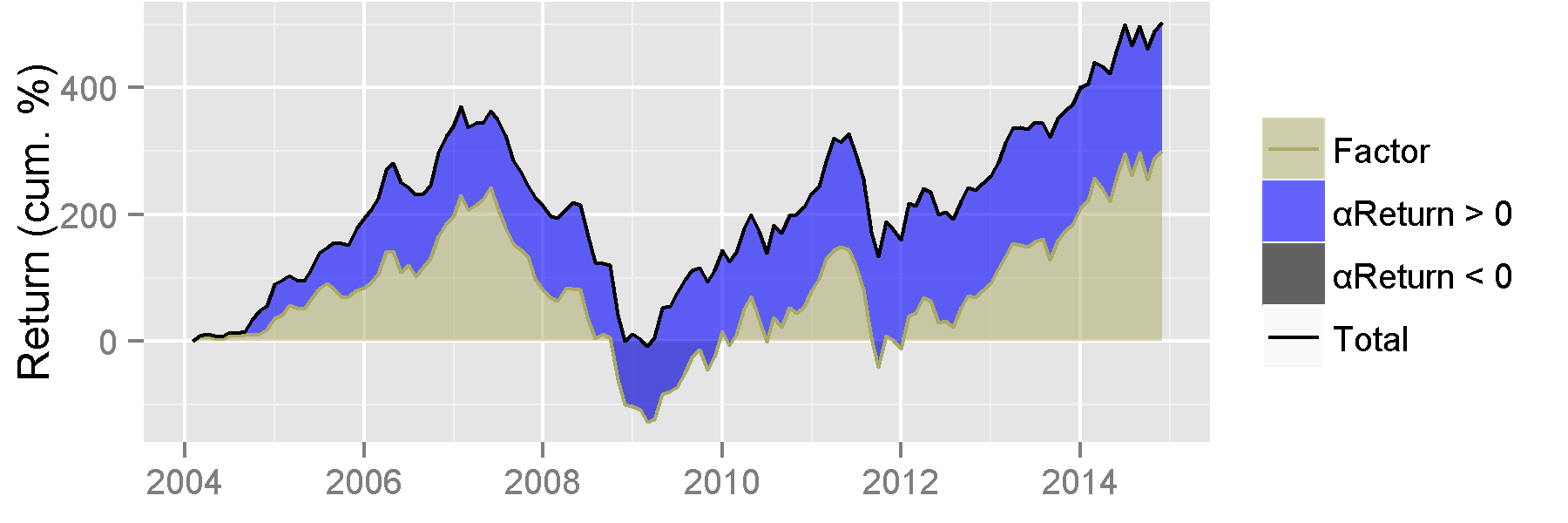

The figures above contrast with those promoted by many data vendors and analytics providers. They typically consider (or provide data on) the survivors only – those funds that are still around, active, and reporting their holdings – HF Surviving Aggregate.

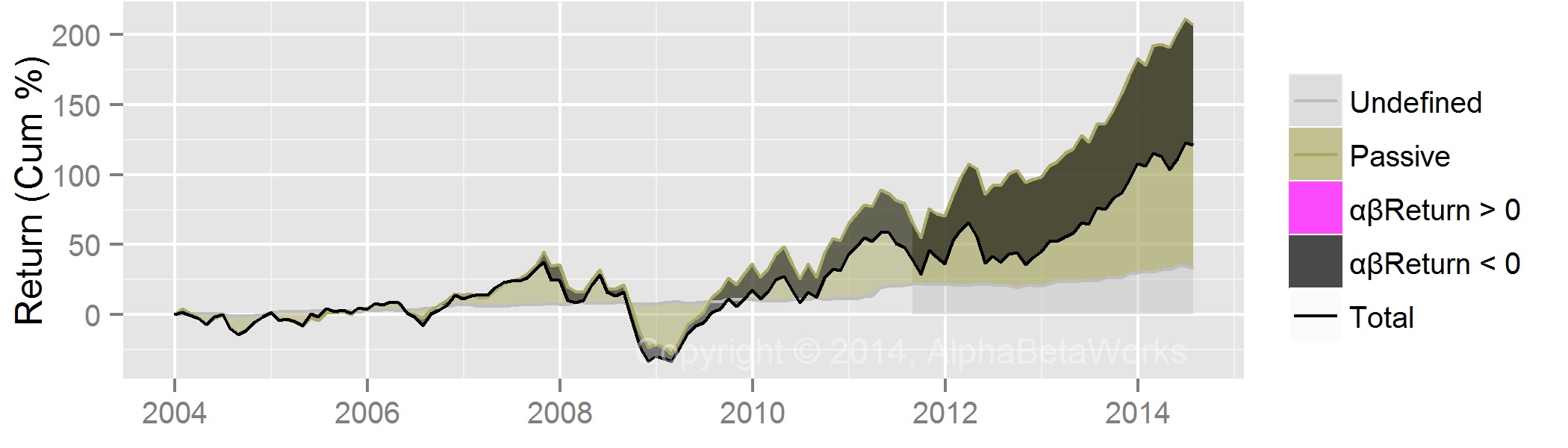

Indeed, the performance of surviving hedge funds is superior: their nominal return is 26% higher than HF Aggregate’s and their security selection performance is positive. Not surprisingly, surviving funds have consistently generated positive risk-adjusted returns from security selection, outperforming the replicating Factor Portfolio. This is the performance investors typically see:

Surviving Medium Turnover U.S. Hedge Fund Long Portfolios: Factor, Residual, and Total Returns

|

Performance (%) |

||

|

Annualized |

10-year |

|

| Total |

9.54 |

159.57 |

| Factor |

9.06 |

147.37 |

| Total – Factor |

0.48 |

12.20 |

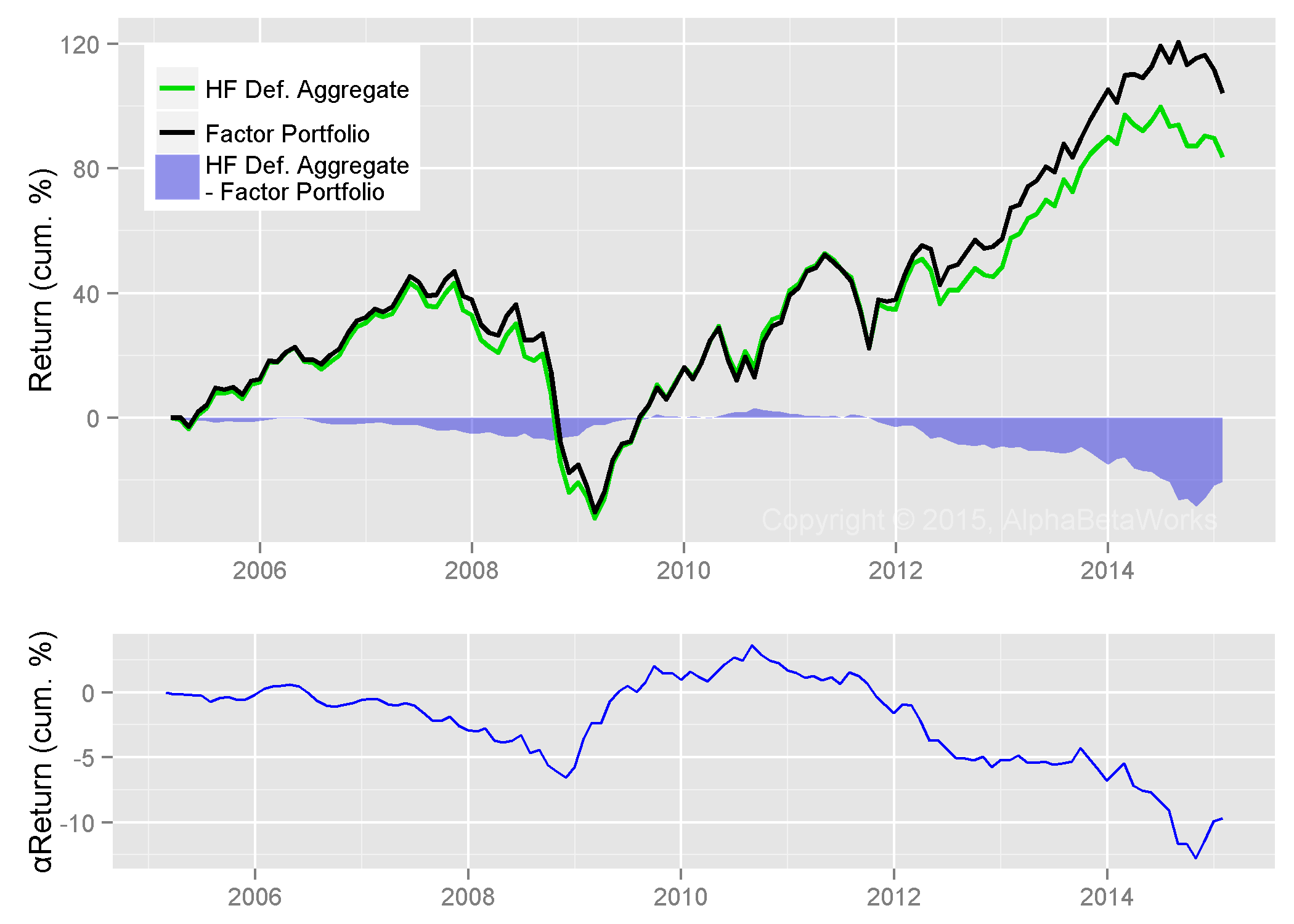

Defunct Hedge Fund Performance

The disconnect between these two pictures of average hedge fund performance is due to survivor bias. Of the approximately 1,000 medium turnover hedge funds tractable using 13Fs that have been active filers over the past 10 years, only half remain. The defunct half dropped out of many databases and out of HF Surviving Aggregate. HF Defunct Aggregate struggled under low factor returns and poor security selection. This is the under-performance swept under the rug:

Defunct Medium Turnover U.S. Hedge Fund Long Portfolios: Factor, Residual, and Total Returns

|

Performance (%) |

||

|

Annualized |

10-year |

|

| Total |

6.07 |

83.52 |

| Factor |

7.14 |

104.12 |

| Total – Factor |

-1.06 |

-20.60 |

The difference in performance between surviving and defunct funds is especially dramatic post-2008:

- Surviving and defunct hedge funds’ long portfolios show similar nominal returns through 2008. Surviving hedge funds are slightly ahead with a 5% higher αReturns.

- The 2008 draw-down for surviving and defunct hedge funds is similar. Both groups generate negative αReturns: widespread portfolio liquidation devastates crowded hedge fund bets across both groups.

- From 2009 the survivors decouple from the defunct: Defunct funds trim exposures. Surviving funds boost exposures.

- Since 2009 HF Surviving Aggregate outperforms HF Defunct Aggregate by over 70%. Approximately half is due to higher systematic risk and half is due to security selection.

- Survival is mostly a matter of exposure and stock picking.

Absent a time machine, investors and fund followers cannot know who will be the future survivors. HF Defunct Aggregate consists of survivors that did well enough to last until 2005, but subsequently perished. Unfortunately, many strategies are built on a swampy foundation – the assumption that the average hedge fund is the same as the average surviving hedge fund. True fund performance is a fifth lower.

Consequently, robust skill analytics developed with the understanding of hedge fund survivor bias are critical to keep investors out of yesterday’s winners that tend to become tomorrow’s losers.

Conclusions

- Historical performance of surviving hedge funds overstates actual average returns by a fifth.

- Hedge fund survivor bias boosts 10-year nominal returns by 26%, primarily post-2008.

- Hedge fund survivor bias boosts 10-year security selection returns by approximately 15%.

- Fund performance and holdings studies that ignore survivor bias will deliver misleading conclusions and disappointing performance.